Top 10 Investment Strategies for Saving Tax in India

Navigating the complex landscape of taxation in India can be challenging, but with careful planning and strategic decision-making, individuals and businesses can significantly reduce their tax liabilities. From utilizing available deductions to leveraging tax-saving investment options, below are a few strategies that can help taxpayers optimize their finances and retain more of their income. Let's explore ten effective strategies to save taxes in India and maximize savings.

Invest in Tax-Saving Instruments:

Take advantage of tax-saving investment options under Section 80C of the Income Tax Act, such as Public Provident Fund (PPF), Equity Linked Savings Schemes (ELSS), National Savings Certificate (NSC), and Tax-Saving Fixed Deposits. Contributions to these instruments qualify for deductions up to Rs. 1.5 lakh per financial year, reducing your taxable income.

Utilize Health Insurance Benefits:

Invest in health insurance plans for yourself and your family to avail deductions under Section 80D. Premiums paid towards health insurance policies are eligible for deductions up to Rs. 25,000 for self, spouse, and dependent children (Rs. 50,000 for senior citizens). Additionally, an additional deduction of up to Rs. 25,000 is available for premiums paid towards parents' health insurance (Rs. 50,000 for senior citizens).

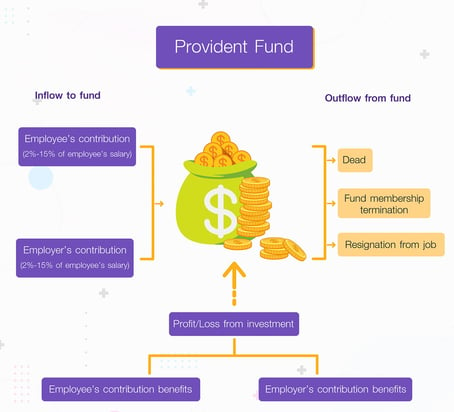

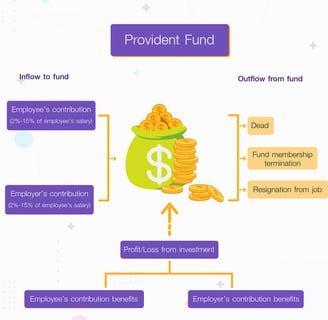

Maximize Contributions to Provident Fund:

Increase your contributions to the Employee Provident Fund (EPF) to maximize tax savings. Employee contributions to EPF are eligible for deductions under Section 80C, up to the prescribed limit of Rs. 1.5 lakh per annum. By contributing more to EPF, you not only save taxes but also build a substantial corpus for your retirement.

Claim House Rent Allowance (HRA):

If you're a salaried individual paying rent, you can claim House Rent Allowance (HRA) to reduce your taxable income. The amount of HRA exemption is determined based on actual HRA received, rent paid, and salary structure. Make sure to provide rent receipts and other supporting documents to claim HRA benefits effectively.

Opt for Home Loan Interest Deduction:

Homebuyers can avail deductions on home loan interest payments under Section 24(b) of the Income Tax Act. The interest paid on a home loan for a self-occupied property is eligible for deductions of up to Rs. 2 lakh per annum. Additionally, first-time homebuyers can claim an additional deduction of up to Rs. 50,000 under Section 80EE for interest on home loans sanctioned between certain specified periods.

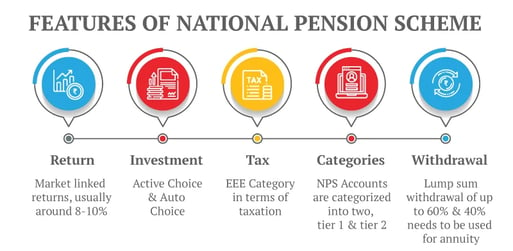

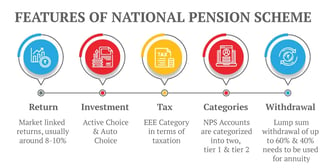

Invest in National Pension System (NPS):

Consider investing in the National Pension System (NPS) to save taxes and build a retirement corpus. Contributions to NPS qualify for deductions under Section 80CCD(1), with an additional deduction of up to Rs. 50,000 available under Section 80CCD(1B). By investing in NPS, taxpayers can enjoy dual benefits of tax savings and long-term wealth creation.

Explore Tax Benefits on Education Expenses:

Parents can avail deductions on tuition fees paid for their children's education under Section 80C. Additionally, interest paid on education loans for higher studies is eligible for deductions under Section 80E. Make sure to retain receipts and certificates from educational institutions to claim these deductions accurately.

Consider Tax-Saving Fixed Deposits (FDs):

Invest in tax-saving fixed deposits offered by banks and financial institutions to earn returns while saving taxes. Tax-Saving FDs have a lock-in period of five years and offer deductions under Section 80C on the invested amount. However, interest earned on these deposits is taxable as per the individual's tax slab rate.

Plan Charitable Contributions:

Make charitable donations to eligible institutions and trusts to avail deductions under Section 80G of the Income Tax Act. Contributions to specified funds, charitable organizations, and government schemes qualify for deductions, subject to specified limits and conditions. Verify the eligibility of the recipient organization and retain donation receipts for claiming deductions.

Maintain Proper Documentation and Compliance:

Ensure compliance with tax laws and maintain accurate records of income, expenses, investments, and deductions. File your income tax returns (ITR) on time and accurately to avoid penalties and scrutiny from tax authorities. Seek professional guidance if needed to optimize tax planning strategies and stay updated on changes in tax regulations.

By implementing these ten tax-saving strategies effectively, taxpayers in India can minimize their tax liabilities and maximize their savings. From investing in tax-saving instruments to leveraging deductions and exemptions, there are ample opportunities to optimize tax efficiency and retain more of your income. Stay informed, plan strategically, and make the most of available tax-saving options to achieve your financial goals while staying compliant with tax laws.